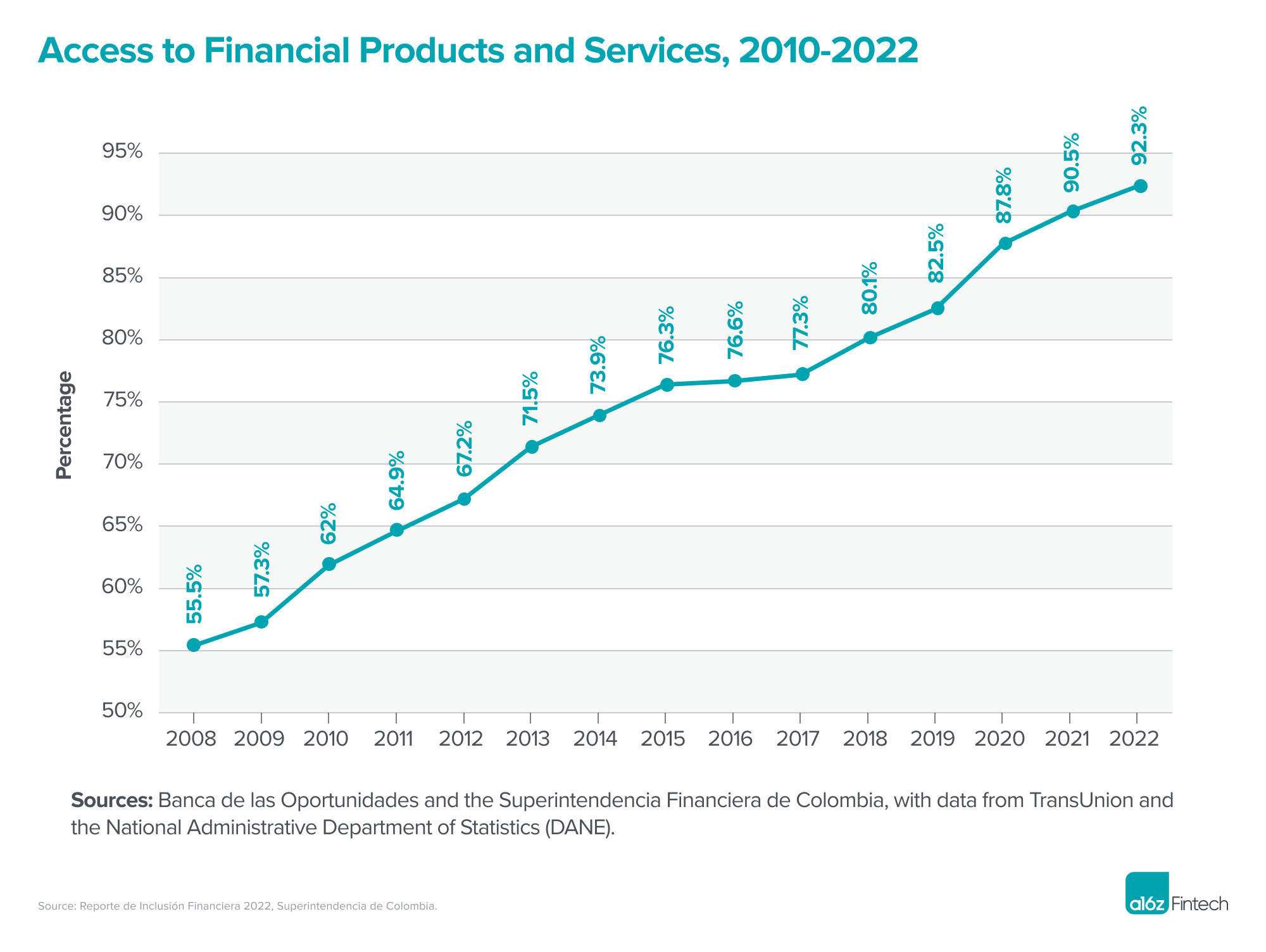

Colombia’s finance sector has historically been one of the most regulated in the world. Over the past decade, however, the country has quietly become the third-largest fintech hub in Latin America (trailing only Brazil and Mexico), home to nearly 300 fintech companies. Seventy-six percent of Colombians use fintech services, according to an Ernst & Young report, the highest fintech adoption rate in Latin America, and from 2008 to 2022, the percentage of Colombian adults who hold a banking product rose from 55% to over 90%.

Given that the majority of Colombians now have access to a smartphone, the internet, and a basic bank account, the conditions are set for an acceleration of financial innovation and inclusion. That trend is being reinforced by advances in licensing and Open Finance, the promise of ubiquitous instant payments, and regulatory support for innovative fintech solutions.

In particular, several government actions have

expanded fintech’s capabilities in Colombia in recent years.

De novo licenses spur market competition

For years, it was difficult and expensive to obtain a de novo banking license in Colombia, a response to the government’s historic struggle to tamp down drug trafficking and money laundering. Today, the banking sector in Colombia remains highly concentrated: there are only 29 fully-licensed banks (establecimientos de credito), and the three largest banking conglomerates control over 60% of deposits, according to the International Monetary Fund.

However, a few years ago the Superintendencia

Financiera de Colombia, the local regulator, opened up the market by introducing

what’s known as a Compania de Financiamiento license. This license has lighter

capital and regulatory requirements, while still allowing its holder to gather

deposits via savings or electronic deposit accounts, offer loans backed by these

deposits, and issue cards.

Since then, fintech companies including Rappi, Uala,

Bold, Mercado Pago, and Nubank have received approval to offer deposit,

transaction, and credit accounts. Not only does this allow new entrants to offer

a comprehensive suite of financial products (and capture the full economics that

lead to sustainable business models), it also gives Colombian consumers greater

confidence that new entrants can be trusted with their money.

Open banking expands

access and inclusion

Alongside opening the market to new entrants, the

government has also committed to developing a robust Open Finance framework, following Brazil’s example. Last year, the government included Open Finance in

its National Development Plan, a foundational law that sets the economic

development program for the next four years. If fully implemented, this will

allow Colombians to own and access their banking data regardless of which

institution they bank with. In addition, the government has signaled an openness

to the potential for full bank account portability, allowing people to migrate

account information between banks, just like they do their cell phone numbers

when they switch carriers.

Instant, interoperable payments will accelerate digitization

Following the success of Pix in Brazil, the Colombian

government has committed to launching its own version of an instant, interoperable and free payment system

in the next two years. Recently, the Central Bank governor (who regulates

payments) indicated that they will announce the technology partner by October of

this year, and that they expect the system to be live before the end of 2024.

Considering that most interbank payments still carry meaningful costs (up to $2

per payment), this will be a boon for the further digitization of payments in

the country.

The future of fintech in Colombia

In Colombia, fintech continues to expand its

reach—the industry is estimated to be growing at around 120% a

year, and the number of fintech companies in the country has more than doubled in the past five years.

Through recent government actions, Colombia is moving toward a more open and transparent financial system—one where a greater number of fintech companies compete to earn users’ trust, money, and business based on the quality of their products and services. The new superintendent has reaffirmed the government’s commitment to an inclusive agenda that fosters competition and innovation. Now it’s up to founders and entrepreneurs to seize the moment by continuing to build the products that will power the future of banking and finance in Colombia.

See a16z.com/global-payments for more.