How Are Consumers Using Generative AI?

It’s been 9 months since ChatGPT was released and 7 months since it became the fastest consumer application to reach 100 million monthly active users, ushering in a new era of generative AI.

But other than ChatGPT, how are consumers interacting with generative AI (GenAI) products? In which categories do incumbents dominate—and where are new companies breaking out? Who might be the next “big winner”?

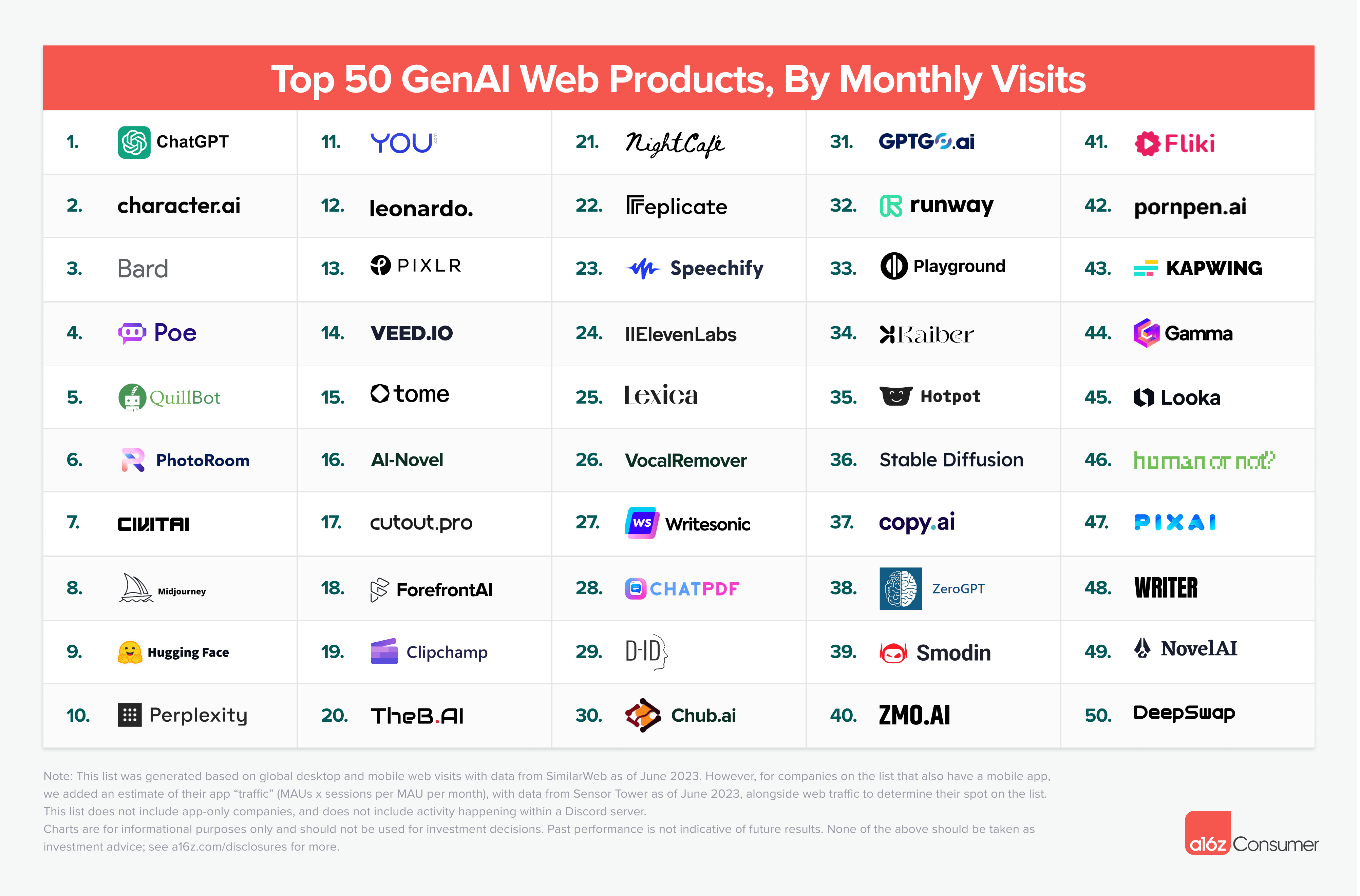

To begin to answer these questions, we looked at SimilarWeb traffic data (as of June 2023) to rank the top 50 GenAI web products by monthly visits. We also analyzed how these products have grown over time, and where growth is coming from.

We relied on web traffic vs. app traffic to “qualify” companies for the list, as most consumer GenAI products have been website-first so far (more on this below!). For companies that made the list that do have a mobile app, we added that traffic, gathered from Sensor Tower as of June 2023, to determine their spot number. Thus, this ranking serves as a tool to identify and understand category trends, and not as an exhaustive ranking of all consumer AI platforms.

Here are our top 6 takeaways.

Note: This list was generated based on global desktop and mobile web visits with data from SimilarWeb as of June 2023. However, for companies on the list that also have a mobile app, we added an estimate of their app “traffic” (MAUs x sessions per MAU per month), with data from Sensor Tower as of June 2023, alongside web traffic to determine their spot on the list.

This list does not include app-only companies, and does not include activity happening within a Discord server.

1. Most leading products are built from the “ground up” around generative AI

Like ChatGPT, the majority of products on this list didn’t exist a year ago—80% of these websites are new. This suggests that while many legacy companies are augmenting their products with AI, many of the most compelling consumer experiences are completely novel.

Of the 50 companies on the list, only 5 are products of, or acquisitions by, pre-existing big tech companies: Bard (Google), Poe (Quora), QuillBot (Course Hero), Pixlr (123RF), and Clipchamp (Microsoft).

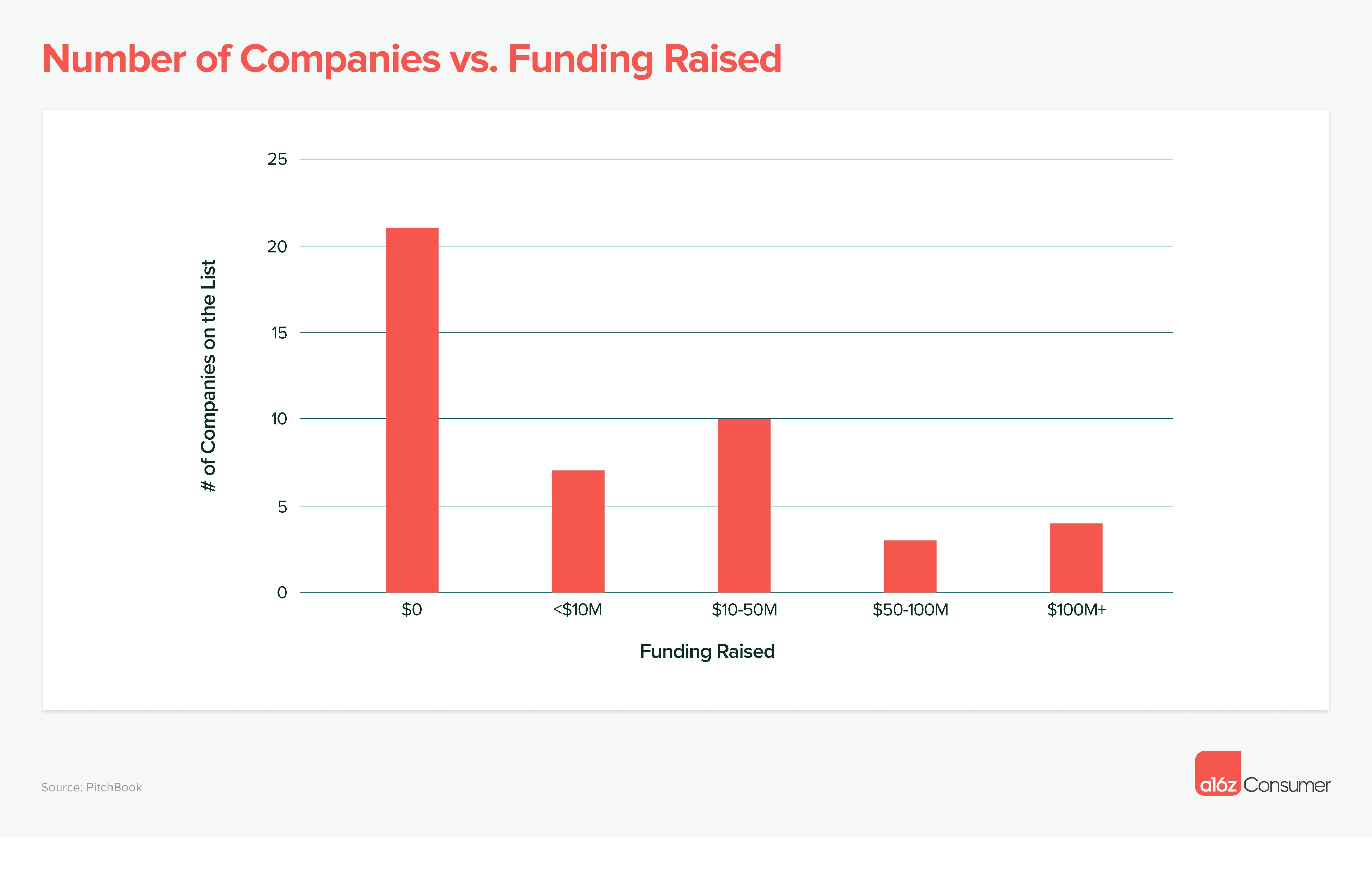

Of the remaining list members, a whopping 48% are completely bootstrapped, with no outside funding, according to PitchBook data. This suggests that it’s possible to get a large AI product off the ground quickly, and with relatively little capital—though another 15% have raised upwards of $50 million already!

One of the main differences between VC-backed and bootstrapped companies? The tech stack. Depending on the model size, setting up and training your own model can cost millions of dollars.

The top 50 list is an almost even 3-way split between companies that (1) trained their own proprietary model, (2) fine-tuned an existing model, and (3) built a consumer UI on top of an existing model (e.g., “GPT wrappers”). However, it’s worth noting that of the top 10 products, half are built on their own model, while 4 are fine tunes—only one falls in the “wrapper” category.

Excluding ChatGPT (which skews the data given OpenAI’s $11.3 billion raised), companies with a proprietary model have raised an average of $98 million. This compares to $20 million for companies that have fine-tuned an open-source model, and $9 million for “wrapper” companies.

2. ChatGPT has a massive lead, for now…

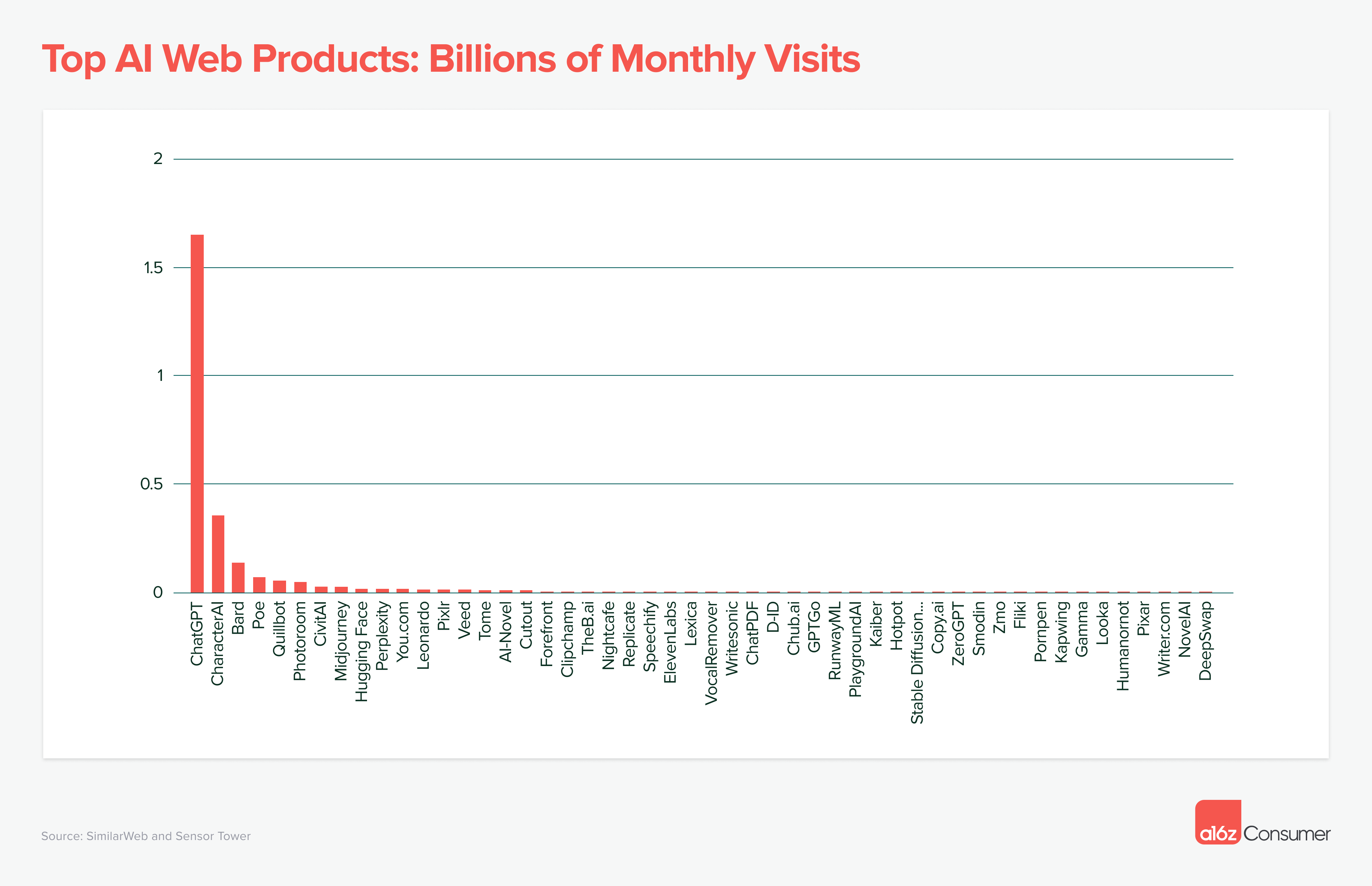

ChatGPT represents 60% of monthly traffic to the entire top 50 list, with an estimated 1.6 billion monthly visits and 200 million monthly users (as of June 2023). This makes ChatGPT the 24th most visited website globally.

No other product has seen quite the same ramp, though companion platform CharacterAI has emerged as a solid #2, with ~21% of the scale of ChatGPT. On mobile in particular, CharacterAI is one of the strongest early players—with DAUs rivaling ChatGPT, and significantly better retention, according to Sensor Tower data.

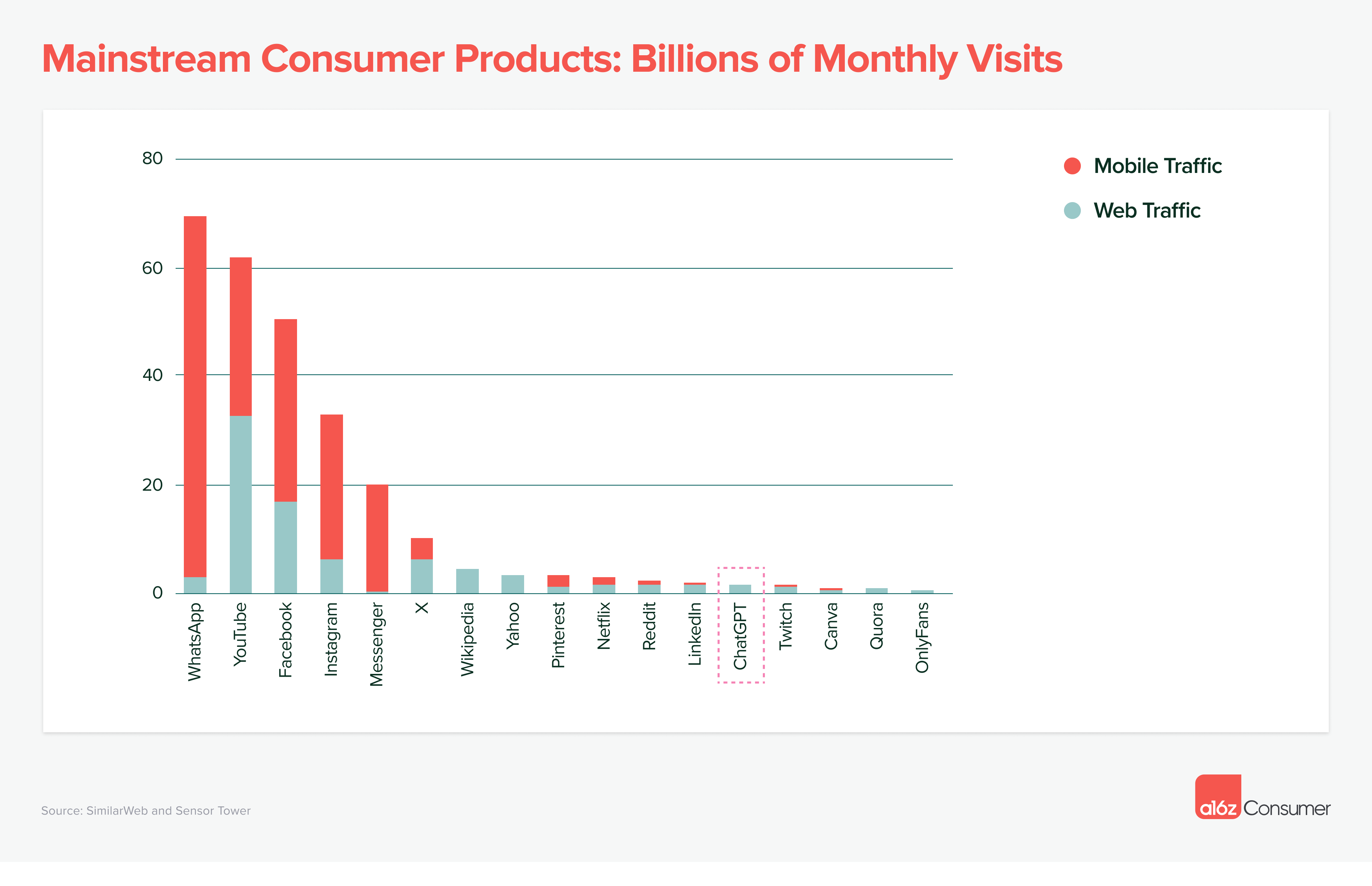

Compared to mainstream consumer products, even the biggest GenAI products are still fairly small. When combining web and mobile app traffic, ChatGPT ranks around the same scale as Reddit, LinkedIn, and Twitch—but still far below the “giants” (WhatsApp, YouTube, Facebook, etc.).

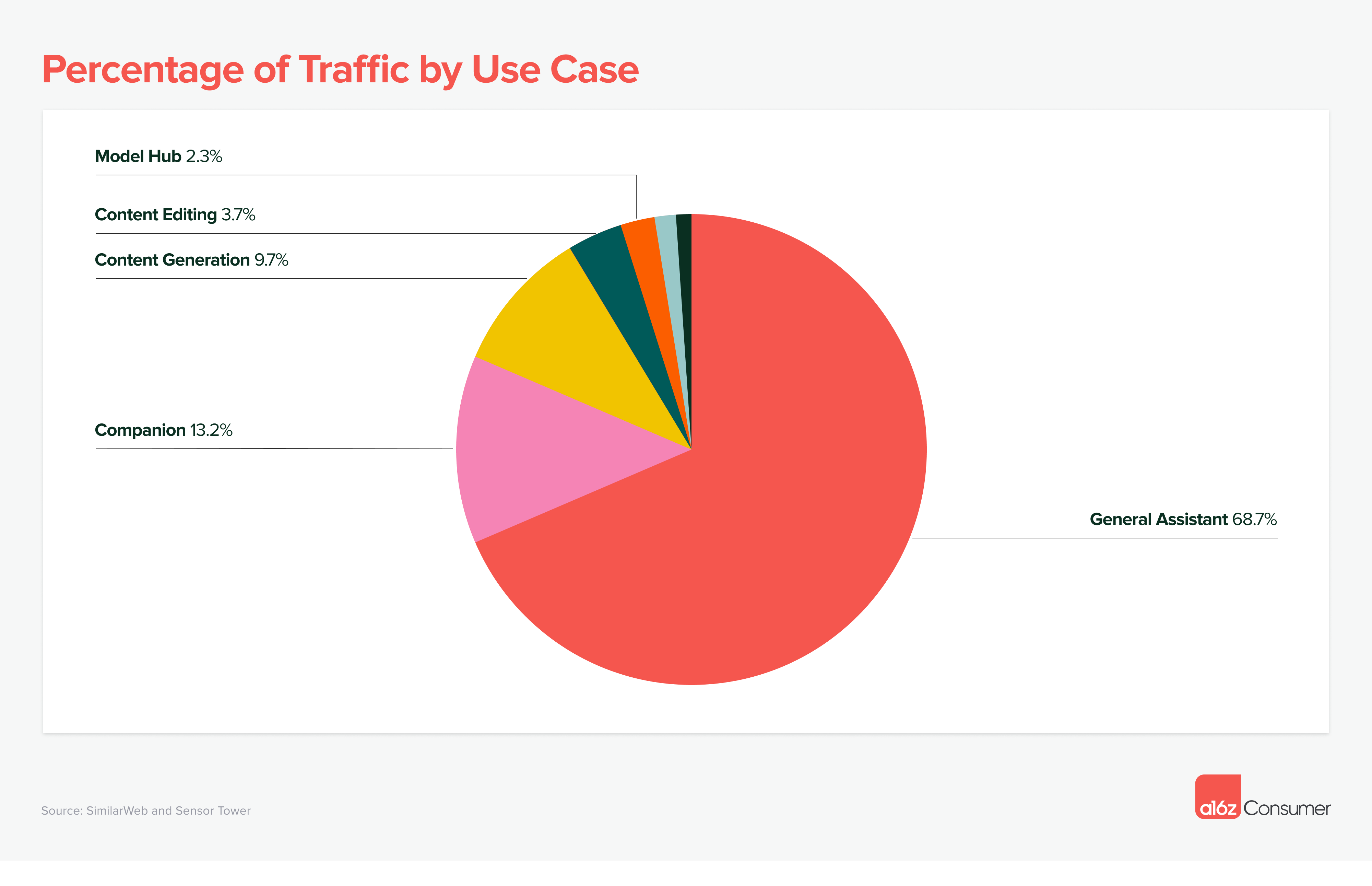

3. LLM assistants (like ChatGPT) are dominant, but companionship and creative tools are on the rise

General LLM chatbots represent 68% of total consumer traffic to the top 50 list. Alongside ChatGPT, this category includes Google’s Bard and Quora’s Poe, all ranked in the top 5.

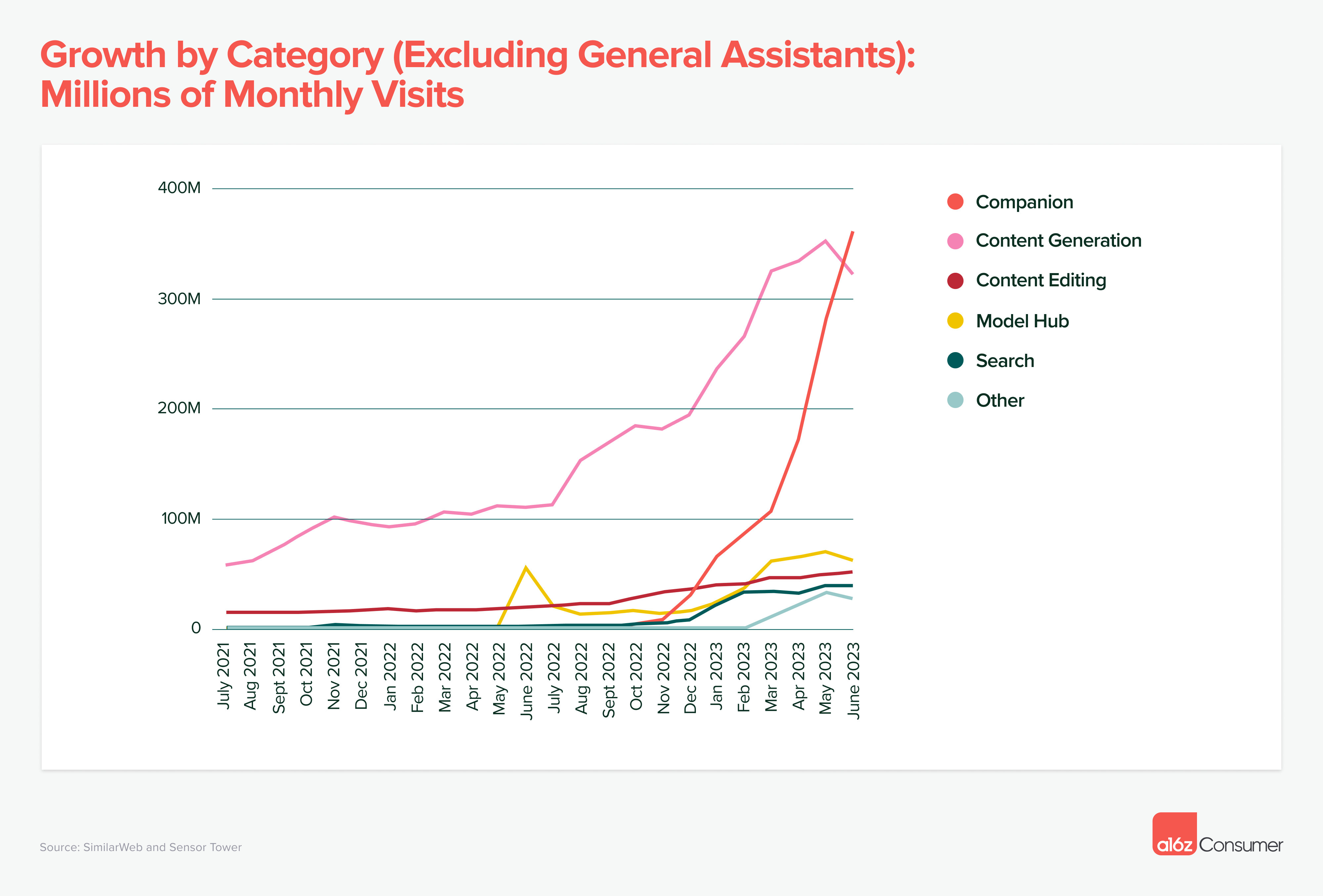

However, two other categories have started to drive significant usage in recent months—AI companions (such as CharacterAI) and content generation tools (such as Midjourney and ElevenLabs). Within the broader content generation category, image generation is the top use case with 41% of traffic, followed by prosumer writing tools at 26%, and video generation at 8%.

Another category worth mentioning? Model hubs. There are only 2 on the list, but they drive significant traffic—Civitai (for images) and Hugging Face both rank in the top 10. This is especially impressive because consumers are typically visiting these sites to download models to run locally, so web traffic is likely an underestimate of actual usage.

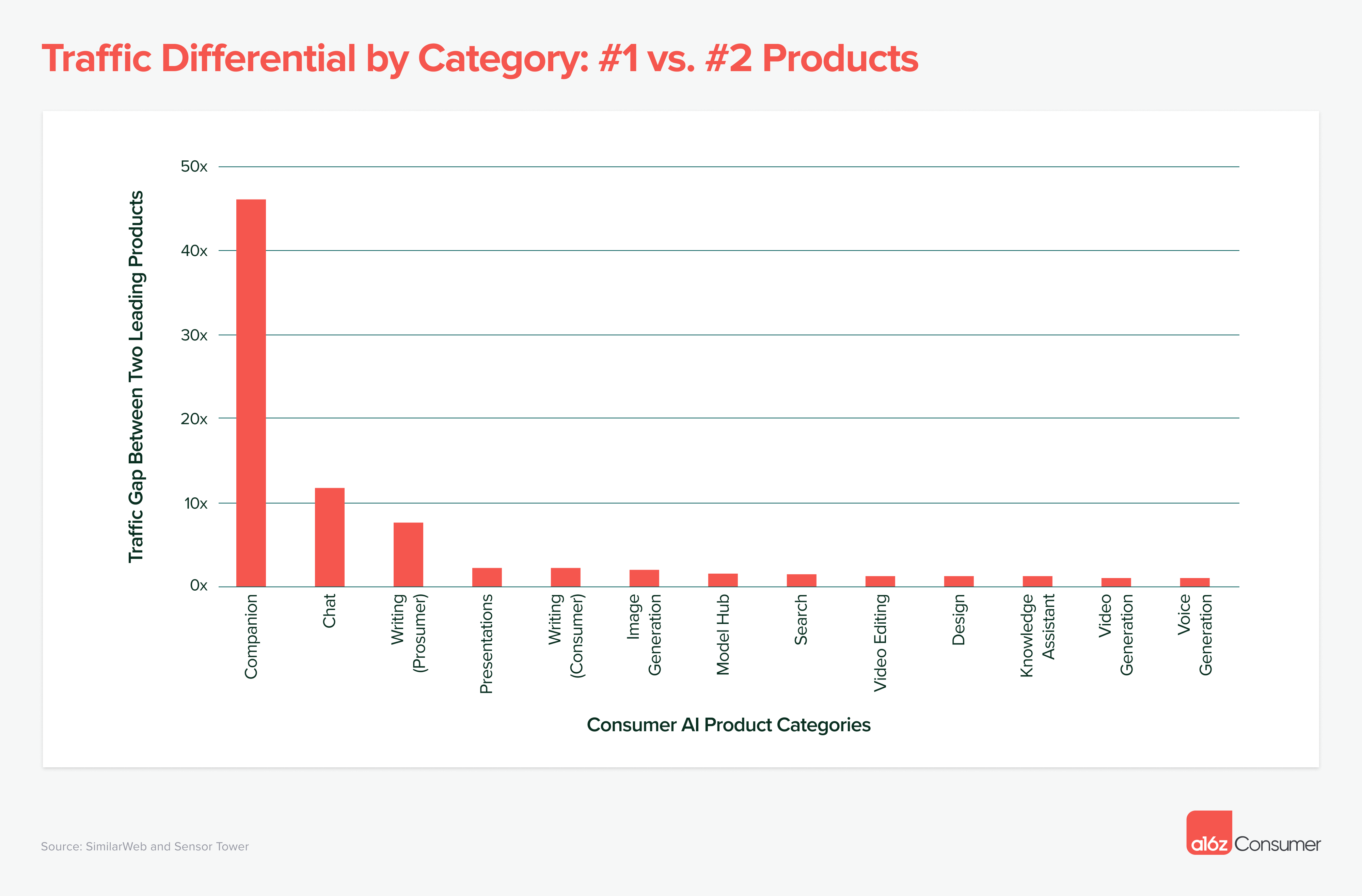

4. Early “winners” have emerged, but most product categories are up for grabs

Good news for builders: despite the surge in interest in generative AI, in many categories there is not yet a runway success.

The below graph shows the differential in traffic between the #1 and #2 players in each space. While there are some exceptions (e.g., companionship), for most categories there is less than a 2x gap—meaning the top company receives just double (or less) the number of visits as its next closest competitor. This is nowhere near insurmountable given companies on the list averaged 50% monthly growth over the past 6 months.

We’re also starting to see significant fragmentation. Products that are purpose-built for specific use cases or workflows are growing alongside more generalist tools, and showing signs that they can also become successful companies.

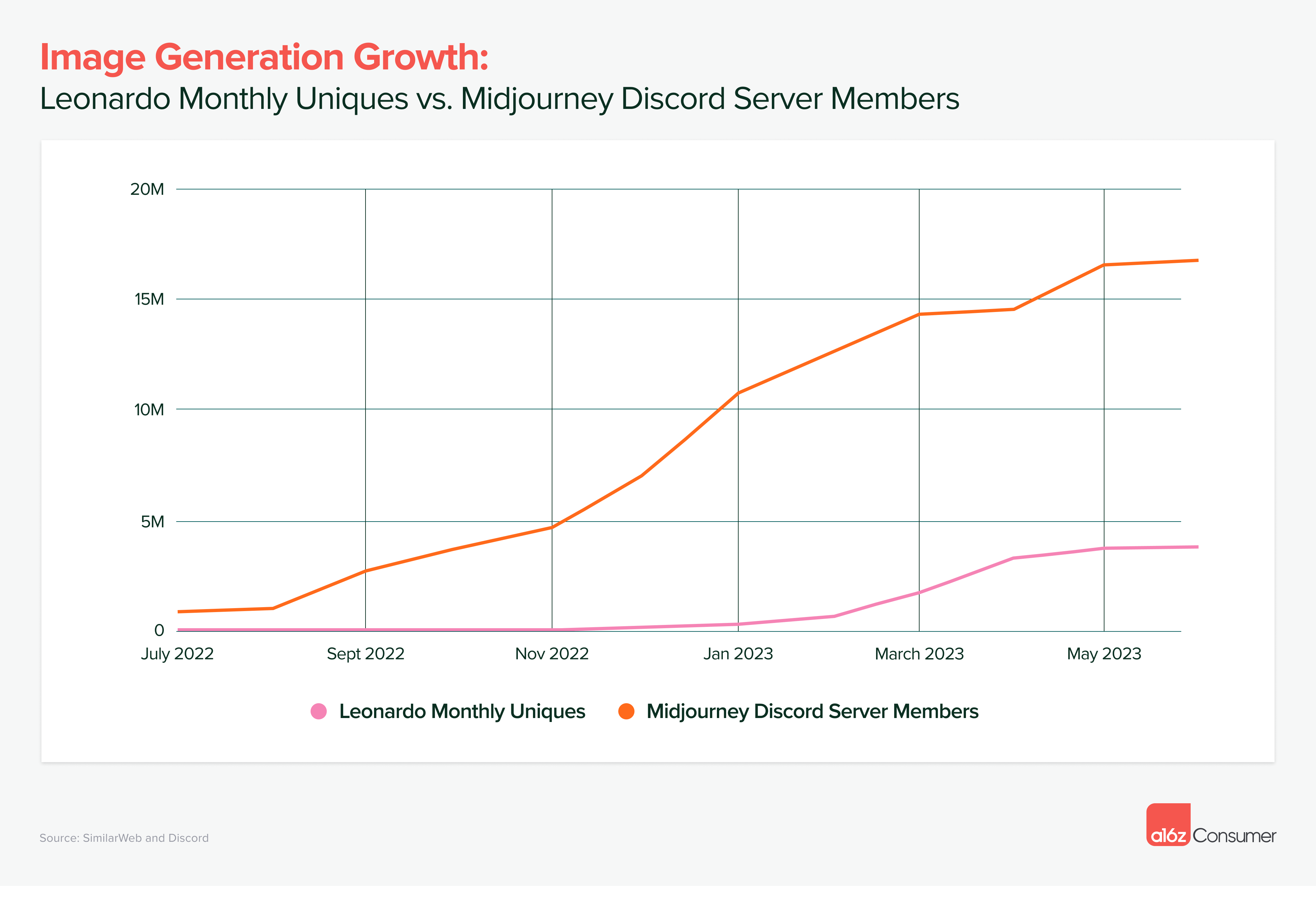

One example is image generation. While Midjourney dominates the broader space, companies like Leonardo (specific to gaming assets) are also seeing impressive growth in traffic. The graph below shows the ramp in Midjourney’s Discord server members, as compared to Leonardo’s monthly unique visitors. While not at the same scale, Leonardo has been able to pick up millions of users alongside Midjourney’s continued ascent.

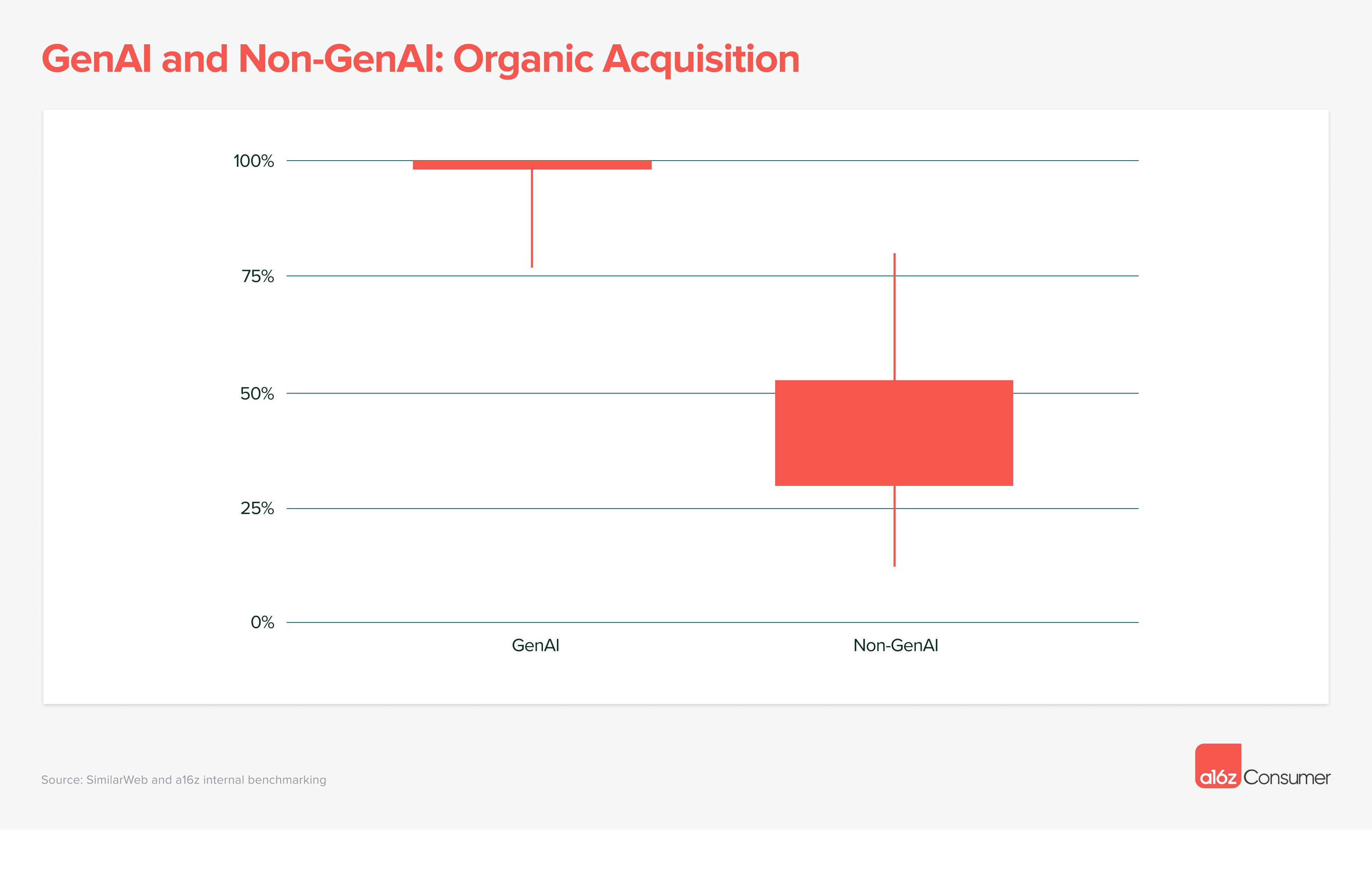

5. Acquisition for top products is entirely organic—and consumers are willing to pay!

For the past 5 years, many consumer apps have been caught in an acquisition game. With no platform shift (e.g., internet → mobile), it’s been difficult to drive excitement for new products. Costs of acquisition have also been rising, meaning that most consumer companies have had to worry about metrics like lifetime value and customer acquisition cost.

GenAI has changed the game. The majority of companies on this list have no paid marketing (at least, that SimilarWeb is able to attribute). There is significant free traffic “available” via X, Reddit, Discord, and email, as well as word of mouth and referral growth.

The bottom quartile of these GenAI products saw just 2% of their traffic coming from paid sources. This compares to 70% paid traffic for the bottom quartile of non-AI consumer subscription companies, per CFI s benchmarking of 150 products.

And consumers are willing to pay for GenAI. 90% of companies on the list are already monetizing, nearly all of them via a subscription model. The average product on the list makes $21/month (for users on monthly plans)—yielding $252 annually.

If you’ve subscribed to any popular consumer subscription products pre-AI (e.g., Calm, Headspace, Duolingo) you’ll know they mostly charge less than $70 per year for annual subscribers—with an average of $10/month for monthly subscribers. Generative AI unlocks a new level of value, which increases consumer willingness to pay.

6. Mobile apps are still emerging as a GenAI platform

Consumer AI products have, thus far, been largely browser-first, rather than app-first. Even ChatGPT took 6 months to launch a mobile app!

There have been notable exceptions. In the image generation category, the “barrier to launch” an app is fairly low, thanks to third-party APIs. Products like Lensa and WOMBO saw steep ascents—and equally steep declines.

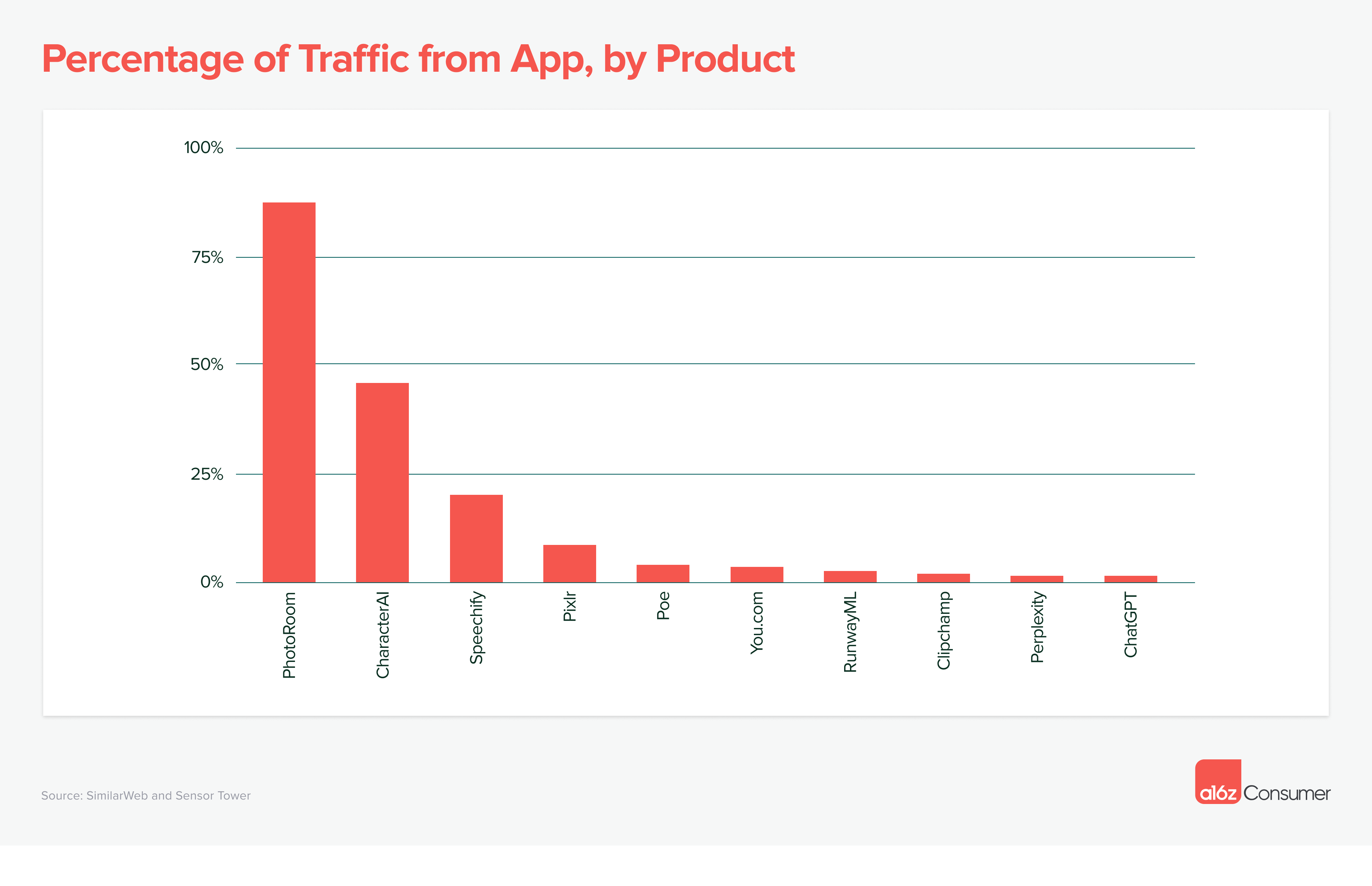

Why aren’t more AI companies building on mobile? The browser is a natural starting place to reach the broadest base of consumers. Many AI companies have small teams and likely don’t want to fragment their focus and resources across Web, iOS, and Android. As a result, only 15 companies on the list currently have a live mobile app, and almost all of them see less than 10% of total monthly traffic come from their app versus the web.

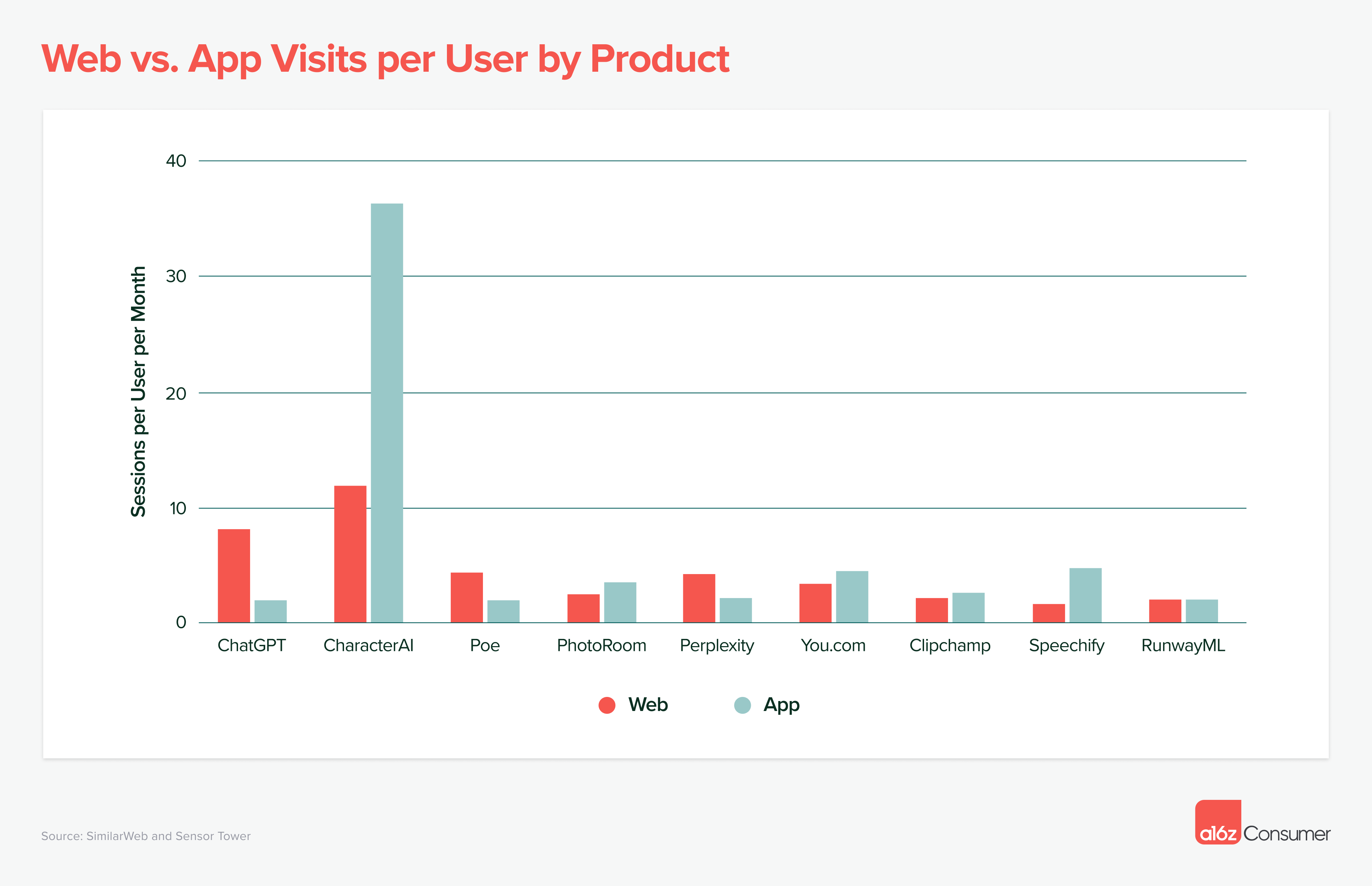

There are 3 notable exceptions: prosumer design studio PhotoRoom (estimated 88% of traffic on app), companion app CharacterAI (46% of traffic on app), and text-to-speech product Speechify (20% of traffic on app). These companies are seeing outsized engagement (measured as sessions per visitor, per month) on their mobile apps, compared to their websites.

Given that the average consumer now spends 36 minutes more per day on mobile than desktop (4.1 hours vs. 3.5 hours), we expect to see more mobile-first GenAI products emerge as the technology matures.

If you’re building something in generative AI, reach out! We’d love to hear from you—you can find me on Twitter at @omooretweets, or via email at omoore@a16z.com.